What is conversion cycle in AIS?

Owen Barnes

Published Feb 02, 2026

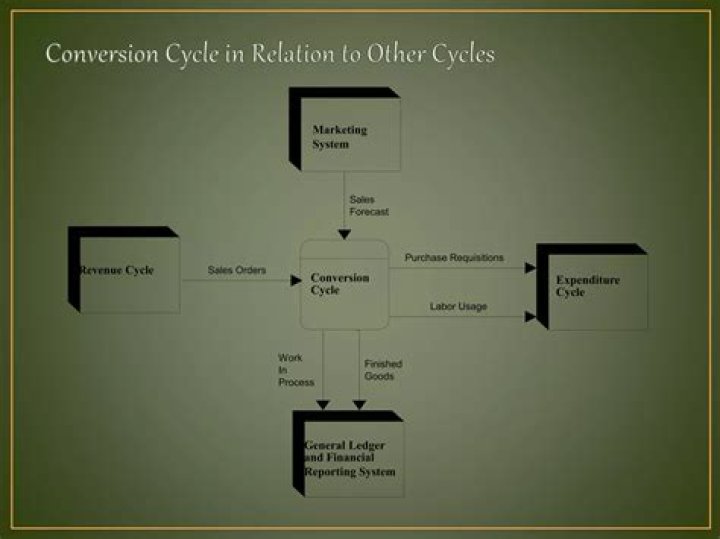

The conversion cycle is one of the four transactions cycle used by accounting systems that records one economic event – the consumption of labor, material and overhead to produce a product or service.

What is the role of conversion cycle?

The cash conversion cycle (CCC) is one of several measures of management effectiveness. It measures how fast a company can convert cash on hand into even more cash on hand.

How do you calculate cash conversion cycle?

The formula for the Cash Conversion Cycle is:

- CCC = Days of Sales Outstanding PLUS Days of Inventory Outstanding MINUS Days of Payables Outstanding.

- CCC = DSO + DIO – DPO.

- DSO = [(BegAR + EndAR) / 2] / (Revenue / 365)

- Days of Inventory Outstanding.

- DIO = [(BegInv + EndInv / 2)] / (COGS / 365)

- Operating Cycle = DSO + DIO.

What is DSO Dio and DPO?

DIO stands for Days Inventory Outstanding. DSO stands for Days Sales Outstanding. DPO stands for Days Payable Outstanding.

What are the key segregation of duties issues in the conversion cycle?

What are the key segregation of duties issues in the conversion cycle? ANS:Inventory control must be separated from raw materials and finished goods custody. Cost accounting must be separate from the work centers. General ledger must be separate from other accounting functions.

Is a negative cash conversion cycle good?

A good cash conversion cycle is a short one. If your CCC is a low or (better yet) a negative number, that means your working capital is not tied up for long, and your business has greater liquidity.

Where is the cash conversion cycle on a balance sheet?

Cash Conversion Cycle = days inventory outstanding + days sales outstanding – days payables outstanding.

What is the difference between cash conversion cycle and operating cycle?

The operating cycle is the number of days between when you buy inventory and when customers pay for the inventory. The cash conversion cycle is the number of days between when you pay for inventory and when you get paid by your customers for the inventory.

What are the risk in converting?

Transfer risk, also known as conversion risk, may arise when a currency is not widely traded and capital controls prevent an investor or business from freely moving currency in or out of a country.

What are the components of cash conversion cycle?

The cash conversion cycle formula has three parts: Days Inventory Outstanding, Days Sales Outstanding, and Days Payable Outstanding.

How do you interpret a negative cash conversion cycle?

Which of the following is an example of transfer risks?

Transferring risk examples include commercial property tenants assuming the risk for keeping sidewalks clear, an apartment complex transferring the risk of theft to a security company and subcontractors assuming the risk for the work they perform for a contractor on a property.